Covid-19 briefing

Powered by

Download GlobalData’s Covid-19 Executive Briefing report

- ECONOMIC IMPACT -

Latest update: 3 December

Omicron threatens to exacerbate inflation and supply chain issues. The Organisation for Economic Co-operation and Development (OECD) has indicated that policymakers should fast-track Covid-19 vaccinations to curb the spread of the new Omicron variant.

The OECD is particularly concerned that the spread of the virus will exacerbate the existing supply-and-demand imbalances that are impacting the global economy, which in turn will risk further fuelling inflation and provide an additional risk to the global economic recovery.

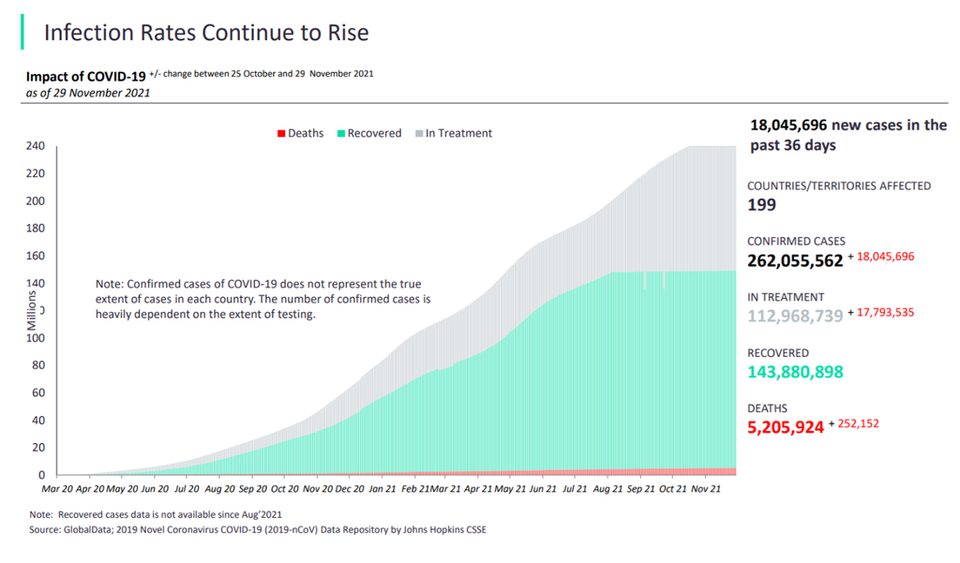

5.2 million

The UK has performed over 5.2 million Covid tests.

33.8%

Positive test rates in Brazil are 33.8%, the highest of any country

Global real GDP growth

% change on previous year

2.6%

-3.7%

5.4%

Pre-Covid-19 2020 forecast

Adjusted 2020 forecast

2021 consensus

forecast

The cost of Covid-19

$375bn

Estimated monthly cost of the Covid-19 pandemic globally

$11tn

Cumulative loss for global economy over the next two years

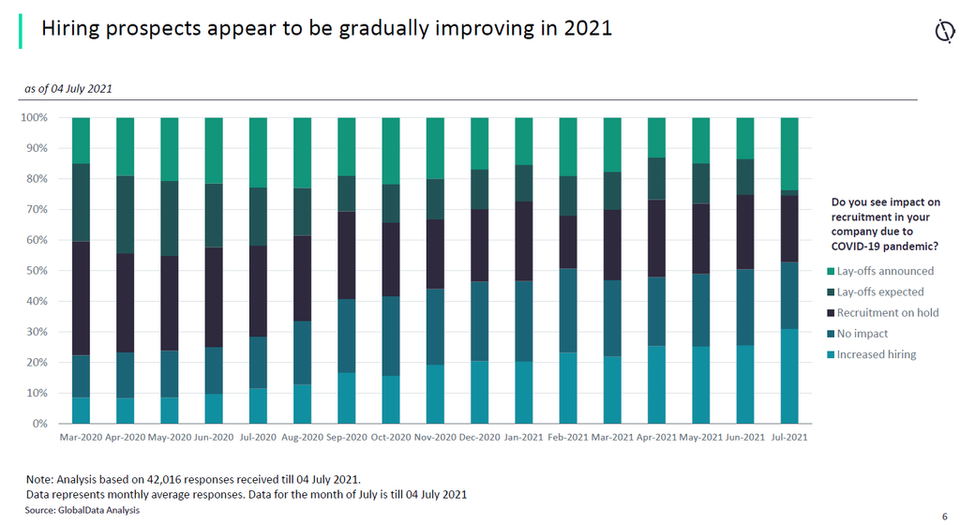

- IMPACT OF COVID-19 ON EMPLOYMENT OUTLOOK -

GlobalData analyses company filings and transcripts, uncovering overarching company sentiment and underlying trends hidden in vast amounts of financial and non-financial data.

Sector indices

GlobalData analyses company filings and transcripts, uncovering overarching company sentiment and underlying trends hidden in vast amounts of financial and non-financial data.

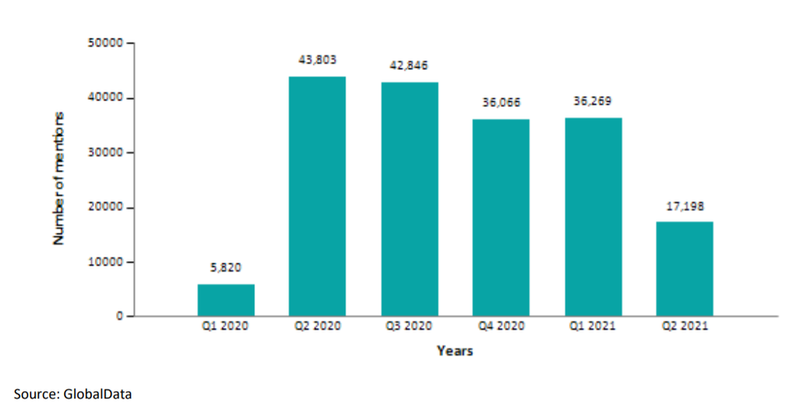

The mentions of COVID-19 in the financial filings of aerospace, defence and security companies grew 7.75% in H1 2021 compared with H1 2020.

- SECTOR IMPACT: AEROSPACE, DEFENCE AND SECURITY -

Last update: 1 December

Airbus now expects commercial aerospace to recover to pre-Covid levels between 2023 and 2025, led by single-aisle extra long-range aircraft. The potential of further lockdowns and travel bans will impact the Primes unevenly, with Boeing having a higher exposure to the faster recovering US domestic market.

Defence markets, although relatively shielded from both immediate demand and supply side shocks, are looking vulnerable in many parts of the world as national debates are ignited around fiscal priorities. However, countries with large domestic capacity are using defence as a stimulus measure and to offset impact in related aerospace markets. Both the US & UK defence markets have seen significant uplift as a result.

The future role of the military in supporting civil contingency planning is also under consideration, as is a redefinition of security to implicitly encompass public health and biosecurity aspects. Western supply chain concerns stemming from Chinese-US rivalry have also been exacerbated by Covid-19. This will result in greater FDI scrutiny, multi-sourcing, and onshoring in key areas such as microelectronics.

Aerospace, Defence and Security Covid-19 mitigation strategies

Military Aerospace

Supply chain disruption from commercial aerospace impact and Covid-19 overall, and possible impact on low TRL-level programmes or legacy support programmes in favour of active production lines as an immediate stimulus measure. Supply chain disruption has potential to resume in face of Omicron, may affect active production lines.

Land platforms

Elements of limited exposure to broader automotive industry supply chains but little impact on programs so far. Higher levels of domestic capability across regions compared to naval and aerospace and less regulated supply chains means future readjustment should be easier and quicker.

C4ISR and electronic warfare

Military Cybersecurity & IT subsectors well positioned in the medium term as a result of demands on distributed working and secure collaboration. Logistic IT specialists also stand to benefit, with new Enterprise Resource Planning (ERP) implementations for supply chain tracking.

Naval shipbuilding

Mostly short-term production challenges. Defense demand impact only extant in medium term.

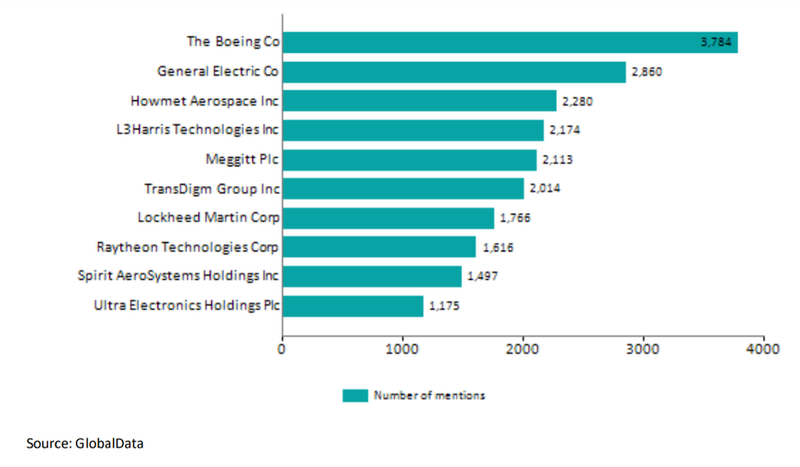

Boeing mentioned Covid-19 more than any other company in the aerospace, defence and security sector during H1 2021.

General Electric held the second position with 2,860 mentions, followed by Howmet Aerospace with 2,280 and L3Harris Technologies with 2,174.

The top ten companies together accounted for 39.8% of total Covid-19-related mentions in the aerospace, defence and security sector.

- SECTOR IMPACT: AEROSPACE, DEFENCE AND SECURITY -

Covid-19-related mentions in the filings of aerospace, defence and security companies rose to 53,467 in H1 2021 from 49,623 in H1 2020.

During the review period Q1 2020 to Q2 2021, the highest number of Covid-19-related mentions in filings were seen in Q2 2020, while Q1 2020 had the least mentions.

Europe occupied the top spot among geography-related mentions of aerospace, defence and security companies discussing Covid-19, followed by Asia-Pacific, North America, and India between Q1 2020 to Q2 2021.

Sub-sector impact

Revenue predictions

Credit: L3Harris